When you think about protecting your family’s future, life insurance probably comes to mind. But did you know there’s a type of policy that does more than just pay out when you die? Cash value life insurance Portugal offers something different—it builds savings while protecting your loved ones. This guide walks you through everything you need to know about this financial tool, from how it works to whether it makes sense for your situation.

What Is Cash Value Life Insurance Portugal

Cash value life insurance Portugal combines two things in one package. First, it provides a death benefit that goes to your beneficiaries when you pass away. Second, it accumulates cash value over time that you can access while you’re still alive. Think of it as insurance that doubles as a savings account.

Unlike term life insurance, which only covers you for a specific period, cash value policies last your entire life as long as you keep paying premiums. The cash portion grows based on how your insurer invests the money or according to a guaranteed rate. You can borrow against this cash, withdraw it, or use it to pay your premiums later on.

Portuguese residents have been increasingly interested in these policies because they offer flexibility that traditional savings accounts don’t provide. The combination of protection and investment makes them attractive for people planning long-term financial security.

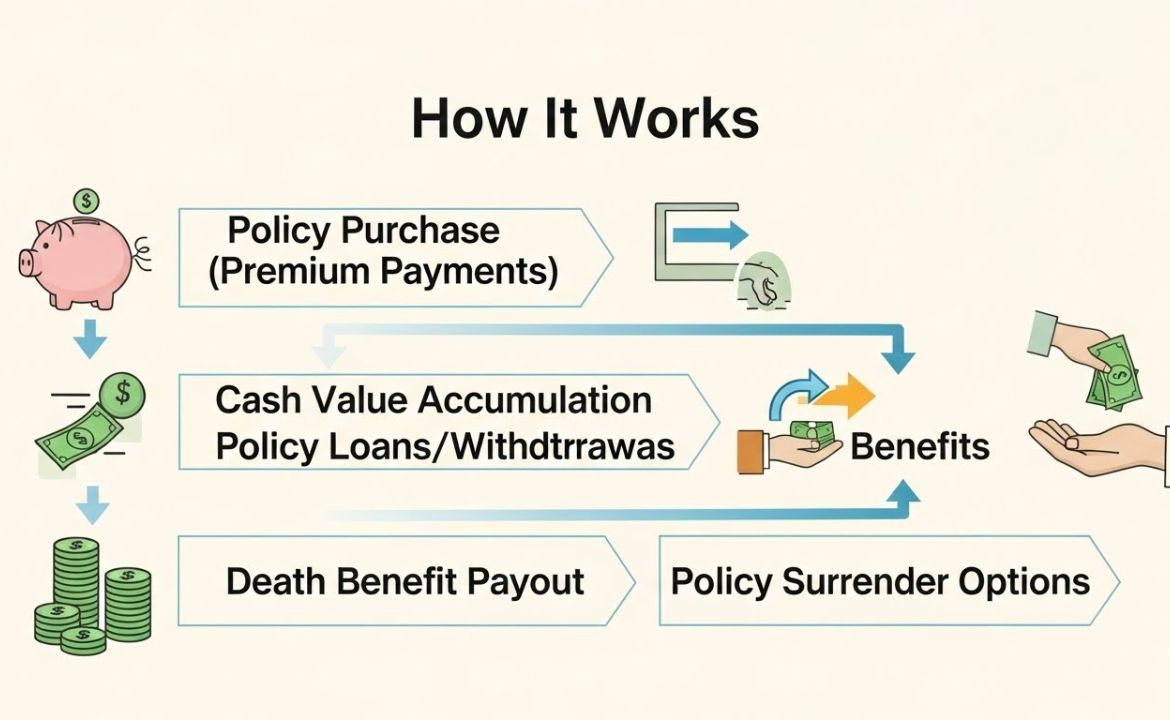

How Cash Value Life Insurance Works in Portugal

The mechanics are straightforward but important to understand. When you pay your premium, the insurance company splits that money. One portion covers the actual insurance cost—the death benefit protection. Another portion goes into the cash value account where it grows over time.

During the early years, most of your premium goes toward insurance costs and company fees. That’s why cash value builds slowly at first. But as time passes, more of your payment goes into the cash account. The growth is typically tax-deferred in Portugal, meaning you don’t pay taxes on the gains until you withdraw them.

There are different types of cash value policies available in Portugal. Whole life insurance offers guaranteed growth rates. Universal life insurance provides more flexibility with premiums and death benefits. Variable life insurance lets you invest the cash value in various funds, though this comes with more risk.

Benefits of Cash Value Life Insurance Portugal

The advantages go beyond simple death benefit coverage. Here’s what makes these policies stand out:

Lifetime Protection: Your coverage doesn’t expire as long as you maintain the policy. You won’t need to reapply or worry about losing coverage when you get older or develop health issues.

Tax Benefits: Portugal offers favorable tax treatment for life insurance policies. The cash value grows without immediate taxation, and death benefits are generally paid to beneficiaries tax-free. This makes Cash Value Life Insurance Portugal an efficient wealth transfer tool.

Flexible Access to Funds: Need money for your child’s education or a business opportunity? You can borrow against your cash value at relatively low interest rates. Unlike traditional loans, you don’t need credit approval since you’re borrowing from yourself.

Retirement Supplement: Many Portuguese residents use their cash value as an additional retirement income source. You can take withdrawals or loans to supplement your pension without triggering the same tax consequences as early pension withdrawals.

Estate Planning Tool: These policies help you leave a legacy for your family while potentially avoiding probate. The death benefit passes directly to your named beneficiaries, making the process simpler during difficult times.

Creditor Protection: Under Portuguese law, life insurance policies often receive protection from creditors. This makes them valuable for business owners or professionals concerned about liability issues.

Costs Associated with Cash Value Life Insurance Portugal

Being honest about costs helps you make better decisions. Cash value life insurance Portugal typically costs more than term life insurance—sometimes five to ten times as much for the same death benefit amount.

Your premiums depend on several factors. Age plays a huge role—buying at 30 costs significantly less than buying at 50. Health status matters too. Smokers pay more than non-smokers. Your occupation and lifestyle choices also influence pricing.

Beyond premiums, you’ll encounter various fees. Administrative charges cover the company’s operating costs. Mortality charges pay for the actual insurance protection. Investment management fees apply if your policy has investment components. Surrender charges hit you if you cancel the policy early, typically within the first 10 to 15 years.

A 35-year-old non-smoking Portuguese resident might pay anywhere from 150 to 400 euros monthly for a policy with a 200,000 euro death benefit, depending on the insurer and policy type. That same coverage through term insurance might only cost 30 to 50 euros monthly. The difference reflects the savings component and lifetime coverage.

Who Should Consider Cash Value Life Insurance in Portugal

This insurance isn’t right for everyone. It makes the most sense for specific situations and goals.

High-income earners who’ve maxed out other retirement savings options often benefit. If you’re already contributing the maximum to your pension funds and still want tax-advantaged savings, these policies provide another avenue.

Business owners find value in using permanent life insurance for succession planning. The policy can fund buy-sell agreements or provide liquidity to pay estate taxes without forcing the sale of business assets.

Parents wanting to leave a guaranteed inheritance regardless of market conditions appreciate the certainty these policies offer. Unlike investments that can lose value, the death benefit provides a known amount.

People with dependents who have special needs see these policies as crucial. The death benefit can fund a special needs trust that provides for a disabled child after the parents pass away.

Young professionals with high future earnings potential sometimes buy policies early to lock in low rates and build cash value over decades. Starting at 25 versus 45 makes a dramatic difference in long-term accumulation.

Comparing Cash Value vs Term Life Insurance Options

Understanding the differences helps you choose wisely. Term life insurance covers you for a specific period—usually 10, 20, or 30 years. It’s pure protection with no savings component. If you don’t die during the term, the policy expires and you get nothing back.

Cash Value Life Insurance Portugal stays in force for life and accumulates savings. Term costs less initially but offers less flexibility. You might pay 40 euros monthly for a 20-year term policy with a 250,000 euro benefit. The equivalent whole life policy might run 300 euros monthly.

Many financial advisors suggest buying term insurance and investing the difference yourself. This strategy works if you have the discipline to consistently invest and can match the returns. However, the forced savings aspect of cash value policies helps people who struggle with regular investing.

Some Portuguese residents use a combination approach. They buy term insurance for immediate high coverage needs during working years, then maintain a smaller permanent policy for final expenses and legacy planning.

Tax Implications for Portuguese Residents

Portugal’s tax treatment of life insurance makes these policies particularly attractive. The cash value growth typically escapes annual taxation. You only pay taxes when you withdraw money, and even then, only on the gains portion.

Death benefits pass to beneficiaries free from income tax in most cases. This differs from other assets that might trigger inheritance taxes. The tax-free transfer makes life insurance an efficient estate planning tool.

If you borrow against your policy rather than withdrawing, you generally don’t trigger any immediate tax consequences. The loan isn’t considered income. However, if the policy lapses with an outstanding loan, you might face unexpected taxes on the gains.

Portuguese tax law can be complex, especially for residents who aren’t Portuguese citizens. Expats living in Portugal should consult with tax advisors familiar with both Portuguese tax law and their home country’s regulations to avoid double taxation issues.

Recent tax reforms in Portugal have maintained favorable treatment for life insurance products, recognizing their role in long-term financial planning. This stability provides confidence for people considering Cash Value Life Insurance Portugal as part of their financial strategy.

Top Insurance Providers Offering Cash Value Policies in Portugal

Several reputable insurers operate in the Portuguese market. International companies like Allianz, AXA, and Zurich have strong presences and offer various cash value products. They bring global expertise and financial stability.

Portuguese companies such as Fidelidade and Tranquilidade understand the local market well and often tailor products specifically for Portuguese residents. They may offer better customer service in Portuguese and understand local regulatory nuances.

When choosing a provider, look beyond just premiums. Financial strength ratings from agencies like A.M. Best or Standard & Poor’s indicate whether the company can pay claims decades from now. Customer service quality matters because you’ll potentially deal with this company for life.

Product options vary by insurer. Some specialize in traditional whole life policies with guaranteed returns. Others focus on universal life products with more flexibility. Variable life offerings appeal to people comfortable with investment risk.

Reading policy documents carefully before signing prevents surprises. Terms regarding loans, withdrawals, and surrender charges differ significantly between companies. A good insurance advisor can explain these details and help you compare options objectively.

Common Mistakes to Avoid When Buying Cash Value Insurance

People make several recurring errors when purchasing these policies. The biggest mistake is buying too much coverage. Getting swept up in sales presentations, some people commit to premiums they can’t sustain long-term. Lapsing a policy after paying for years means losing much of what you invested.

Another error is focusing only on the cash value and ignoring the death benefit. Remember that protection for your family is the primary purpose. The savings component should be secondary.

Many buyers don’t understand the fees and charges. Surrender charges can be substantial if you need to cancel within the first decade. These penalties can eliminate much of your cash value. Always ask about surrender schedules before committing.

Failing to compare options across multiple insurers costs money. Premiums and cash value growth rates vary considerably. Getting quotes from at least three different companies helps ensure you’re getting reasonable value.

Some people don’t coordinate their life insurance with their overall financial plan. Cash value policies should complement your retirement accounts, emergency funds, and other investments—not replace them. Working with a financial planner who doesn’t earn commissions from insurance sales can provide objective guidance.

How to Apply for Cash Value Life Insurance in Portugal

The application process isn’t complicated but requires preparation. Start by determining how much coverage you need and how much you can afford monthly. Online calculators can help, but speaking with an advisor provides more personalized guidance.

You’ll complete an application with detailed questions about your health history, lifestyle, occupation, and family medical history. Be completely honest. Lying on your application can void the policy, leaving your beneficiaries without benefits when they need them most.

Most policies require a medical examination. A nurse typically comes to your home or office to check your blood pressure, draw blood, and collect a urine sample. Results go directly to the insurance company’s underwriters.

Underwriters review your application and medical results to assess your risk. This process takes anywhere from a few weeks to a couple months. They’ll assign you a risk class that determines your premium. Excellent health means lower premiums.

Once approved, you’ll review the policy documents and make your first premium payment. Many Portuguese insurers offer bank draft options for convenient automatic payments. The policy becomes active once the first payment clears.

Withdrawing and Borrowing from Your Cash Value

Accessing your money when you need it is one reason people choose Cash Value Life Insurance Portugal. You have several options, each with different implications.

Direct withdrawals reduce both your cash value and death benefit. You can typically withdraw up to your basis—the total premiums you’ve paid—without tax consequences. Withdrawals beyond your basis trigger taxes on the gains. The death benefit decreases by the withdrawal amount.

Policy loans work differently. You borrow against the cash value while it remains in your account, continuing to grow. You pay interest on the loan, though rates are usually lower than credit cards or personal loans. The loan doesn’t require credit approval or fixed repayment schedules.

If you die with an outstanding loan, the insurance company deducts the loan balance plus interest from the death benefit before paying your beneficiaries. This reduces the inheritance but doesn’t eliminate it entirely.

Some policies offer automatic premium loans if you miss a payment. The company automatically borrows from your cash value to pay the premium, keeping your policy active. This feature prevents accidental lapses but adds to your loan balance.

Strategic use of loans and withdrawals can provide tax-efficient retirement income. By carefully managing when and how much you take, you can supplement other retirement sources while minimizing taxes. A financial advisor experienced with life insurance can help develop this strategy.

Future of Cash Value Life Insurance in the Portuguese Market

The market for these products continues evolving. Portuguese consumers are becoming more financially sophisticated and interested in products that serve multiple purposes. Cash Value Life Insurance Portugal fits this trend by combining protection, savings, and tax benefits.

Digital transformation is changing how people buy insurance. More insurers offer online applications and faster underwriting. Some companies now provide instant decisions for healthy applicants, eliminating the traditional waiting period.

Regulatory changes focus on transparency and consumer protection. Recent European insurance directives require clearer disclosure of fees and charges. This helps buyers make more informed comparisons between policies and providers.

Product innovation brings new options. Hybrid policies that combine long-term care benefits with life insurance are gaining popularity. These policies pay out if you need nursing home care or assisted living, not just upon death.

Environmental and social considerations are influencing investment options within variable policies. Some insurers now offer sustainable investment funds within their cash value products, appealing to socially conscious buyers.

Making Your Decision: Is Cash Value Life Insurance Right for You

Deciding whether to buy requires honest assessment of your situation. Consider your current financial position, long-term goals, and family responsibilities. Are you disciplined enough to invest consistently if you don’t buy cash value insurance? Do you need forced savings mechanisms?

Think about your time horizon. These policies work best over decades. If you’re in your late 50s or 60s, the benefits might not justify the costs compared to other options. Younger buyers have time to build substantial cash value.

Evaluate your other insurance coverage and retirement savings. If you don’t have adequate term life insurance covering your family’s immediate needs, start there before considering cash value policies. If your retirement accounts aren’t maxed out, prioritize those first.

Talk to multiple advisors. Get opinions from fee-only financial planners who don’t sell insurance, as well as insurance professionals. Comparing perspectives helps you see the complete picture.

Request illustrations showing exactly how your policy would perform under different scenarios. Look at guaranteed values versus projected values. The guaranteed numbers are what you can count on; projections depend on assumptions that might not materialize.

Take your time making this decision. Don’t let anyone pressure you into buying before you’re ready. A good insurance advisor will respect your need to think things through and compare options thoroughly.

Conclusion

Cash Value Life Insurance Portugal offers a unique combination of protection and savings that appeals to many residents planning their financial futures. These policies provide lifetime coverage, tax-advantaged growth, and flexible access to funds. However, they cost significantly more than term insurance and work best for people with specific long-term goals and the ability to maintain premiums for decades.

Understanding how these policies work, their benefits and costs, and how they fit into your overall financial plan is essential before buying. The right choice depends on your age, income, family situation, risk tolerance, and financial objectives. For some Portuguese residents, cash value policies become valuable tools for wealth building and legacy planning. For others, simpler and less expensive options make more sense.

If you’re considering this type of insurance, take the next step by speaking with qualified financial advisors and insurance professionals. Request detailed proposals from multiple insurers, compare the numbers carefully, and ask questions until you fully understand what you’re buying. Your future financial security deserves this level of attention and care.